Exploring the realm of equity loans, this introduction will captivate readers with a comprehensive overview of what equity loans entail, how they function, and the various types available.

As we delve deeper, we will uncover the application process, benefits, risks, and essential tips associated with equity loans, providing a well-rounded understanding of this financial tool.

What is an equity loan?

An equity loan, also known as a home equity loan or a second mortgage, is a type of loan that allows homeowners to borrow money using the equity in their home as collateral. Equity is the difference between the market value of the property and the outstanding balance on the mortgage.

How do equity loans work?

Equity loans work by allowing homeowners to borrow a lump sum of money based on the equity they have built up in their home. The loan is typically repaid over a fixed term with regular monthly payments of principal and interest. If the borrower fails to repay the loan, the lender has the right to foreclose on the property to recover the amount owed.

- Interest rates on equity loans are usually lower than other types of loans because the home serves as collateral, reducing the risk for the lender.

- Equity loans can be used for various purposes such as home renovations, debt consolidation, or funding education.

- Unlike a home equity line of credit (HELOC), which functions more like a credit card with a revolving line of credit, an equity loan provides a one-time lump sum payment.

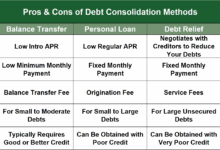

Comparison to other types of loans

Equity loans differ from traditional personal loans in that they are secured by the value of the borrower’s home. This means that if the borrower defaults on the loan, the lender can seize the property to recover their investment. In contrast, personal loans are unsecured and do not require collateral, but typically come with higher interest rates to offset the increased risk for the lender.

| Equity Loan | Personal Loan |

|---|---|

| Secured by home equity | Unsecured |

| Lower interest rates | Higher interest rates |

| Fixed term repayment | Flexible repayment terms |

Types of equity loans

When considering equity loans, it’s essential to understand the different types available to choose the best option for your financial needs. Here are some common types of equity loans, along with their pros and cons:

Home Equity Loan

A home equity loan is a type of loan that allows homeowners to borrow against the equity in their home. This loan is suitable for homeowners who have a significant amount of equity in their property and need a large sum of money for a specific purpose, such as home renovations or debt consolidation.

Pros:

– Fixed interest rates

– Lump sum payment

– Potential tax benefits

Cons:

– Risk of foreclosure if unable to repay

– Closing costs and fees

Home Equity Line of Credit (HELOC)

A HELOC is a revolving line of credit that allows homeowners to borrow money as needed, up to a certain limit, using their home as collateral. This type of equity loan is suitable for homeowners who need access to funds over time for ongoing expenses or projects.

Pros:

– Flexibility to borrow as needed

– Variable interest rates

– Potential tax benefits

Cons:

– Interest rate fluctuations

– Risk of overspending and accumulating debt

Cash-Out Refinance

A cash-out refinance involves refinancing your existing mortgage for a higher amount than you currently owe and taking the difference in cash. This type of equity loan is suitable for homeowners who want to access a large sum of money and potentially secure a lower interest rate.

Pros:

– Consolidation of debt

– Potentially lower interest rates

– Single monthly payment

Cons:

– Resetting of mortgage term

– Closing costs and fees

Shared Equity Agreement

A shared equity agreement involves partnering with an investor who provides funds in exchange for a share of the property’s appreciation. This type of equity loan is suitable for homeowners who want to access cash without taking on additional debt.

Pros:

– No monthly payments

– Potential for property value appreciation

– Diversified investment portfolio

Cons:

– Loss of full equity

– Limited control over property decisions

Applying for an equity loan

When applying for an equity loan, there are specific steps to follow to increase your chances of approval. Understanding the process and being prepared with the necessary documentation can make the application process smoother.

Steps involved in applying for an equity loan:

- Research and compare lenders to find the best terms and rates for your equity loan.

- Check your credit score and work on improving it if necessary to qualify for better loan terms.

- Calculate the amount of equity you have in your home to determine how much you can borrow.

- Fill out the application form provided by the lender with accurate information about your financial status.

- Provide the required documentation to support your application, such as income verification, property appraisal, and debt information.

- Wait for the lender to review your application and make a decision on whether to approve your equity loan.

- If approved, review the terms of the loan carefully before signing the agreement.

Documentation required for an equity loan application:

- Proof of income: Recent pay stubs, tax returns, or bank statements to verify your ability to repay the loan.

- Property appraisal: An appraisal of your home to determine its current market value and the amount of equity available.

- Debt information: Details of any outstanding debts or loans to assess your overall financial situation.

- Identification: Valid ID such as a driver’s license or passport to confirm your identity.

- Insurance: Proof of homeowners insurance to protect the lender’s interest in the property.

Tips for improving the chances of getting approved for an equity loan:

- Maintain a good credit score by paying bills on time and reducing outstanding debt.

- Prepare all necessary documentation in advance to streamline the application process.

- Show stable income and employment history to demonstrate your financial stability.

- Consider a co-signer with a strong credit history to strengthen your application.

- Be honest and accurate in providing information to the lender to avoid delays or rejection.

Benefits of equity loans

Equity loans offer several advantages to homeowners looking to access funds for various expenses. These loans are secured by the equity in your property, making them a viable option for those in need of financial assistance.

1. Lower interest rates

- Equity loans typically come with lower interest rates compared to unsecured loans or credit cards.

- By leveraging the equity in your home, you can secure a loan at a more favorable rate, resulting in lower monthly payments and overall interest costs.

2. Flexible use of funds

- Equity loans provide borrowers with the flexibility to use the funds for a variety of purposes.

- Whether it’s home renovations, debt consolidation, education expenses, or unexpected medical bills, equity loans can help finance these needs.

3. Potential tax benefits

- Interest paid on equity loans may be tax-deductible, depending on the specific circumstances.

- Homeowners should consult with a tax professional to understand the potential tax advantages of taking out an equity loan.

4. Access to larger loan amounts

- Since equity loans are secured by the value of your home, lenders may be willing to offer larger loan amounts compared to unsecured options.

- This can be beneficial when you have significant expenses or projects that require substantial funding.

Risks associated with equity loans

When considering an equity loan, it is essential to be aware of the potential risks involved to make an informed decision.

Potential Risks of Equity Loans

- Interest Rates: Equity loans typically come with variable interest rates, which means your monthly payments can fluctuate based on market conditions.

- Property Value Fluctuations: The value of your home can change over time, impacting the amount of equity you have available for borrowing.

- Foreclosure Risk: If you default on your equity loan payments, you could risk losing your home to foreclosure.

- Additional Fees and Costs: There may be hidden fees and costs associated with equity loans, such as closing costs and appraisal fees, which can add to the overall expense.

Consequences of Defaulting on an Equity Loan

- Damage to Credit Score: Defaulting on an equity loan can significantly damage your credit score, making it challenging to secure credit in the future.

- Loss of Home: In the worst-case scenario, defaulting on an equity loan can lead to foreclosure, resulting in the loss of your home.

- Lawsuits and Legal Action: Lenders may pursue legal action to recover the unpaid debt, leading to potential lawsuits and court judgments against you.

Mitigating Risks with Equity Loans

- Thoroughly Assess Financial Situation: Before taking out an equity loan, assess your financial situation to ensure you can afford the monthly payments.

- Shop Around for the Best Terms: Compare offers from different lenders to find the best terms and interest rates for your equity loan.

- Read the Fine Print: Carefully review the terms and conditions of the loan agreement to understand all fees, costs, and potential risks involved.

- Have a Repayment Plan: Create a repayment plan to ensure you can meet your monthly obligations and avoid defaulting on the loan.

Concluding Remarks

In conclusion, equity loans offer a valuable opportunity for homeowners to leverage their property’s equity for various financial needs. By understanding the nuances of equity loans, individuals can make informed decisions to optimize their financial strategies.