Instant loans offer a fast financial solution in times of need. From understanding the types available to navigating the application process, this comprehensive guide covers all aspects of instant loans.

Definition and Types of Instant Loans

Instant loans are a type of short-term borrowing that allows individuals to access funds quickly, usually within a few hours or even minutes. These loans are designed to provide immediate financial relief for urgent needs, such as unexpected expenses or emergencies. Unlike traditional loans, which may require extensive paperwork and credit checks, instant loans often have minimal requirements and a streamlined application process.

Types of Instant Loans

Instant loans come in various forms to cater to different financial needs. Here are some common types of instant loans available in the market:

- Payday Loans: These are small, short-term loans typically due on the borrower’s next payday. They are quick and easy to obtain but often come with high interest rates.

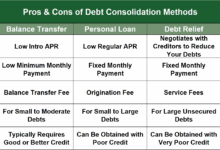

- Personal Loans: Instant personal loans provide a larger amount of money that can be used for various purposes, such as debt consolidation or home improvement projects. They usually have a longer repayment period compared to payday loans.

- Online Installment Loans: These loans allow borrowers to repay the borrowed amount in equal installments over a specified period. They offer flexibility in repayment and may have lower interest rates than payday loans.

- Line of Credit: A line of credit works similarly to a credit card, allowing borrowers to access funds up to a predetermined limit. Interest is only charged on the amount borrowed, making it a flexible borrowing option.

Features and Benefits of Each Type of Instant Loan

Payday Loans: Quick approval process, suitable for emergencies, but high interest rates may lead to a cycle of debt if not managed properly.

Personal Loans: Higher loan amounts, longer repayment terms, and lower interest rates compared to payday loans. Ideal for larger expenses or debt consolidation.

Online Installment Loans: Flexible repayment options, lower interest rates, and predictable monthly payments. Suitable for borrowers who need to borrow a larger amount and repay it over time.

Line of Credit: Access to funds as needed, only pay interest on the amount borrowed, and flexible repayment terms. Great for managing fluctuating expenses or unexpected costs.

Application Process

When applying for an instant loan, the process typically involves the following steps:

Submission of Online Application

- Applicants need to fill out an online form on the lender’s website with personal and financial information.

- Details required may include name, address, contact information, employment status, income, and banking details.

Verification of Information

- Once the application is submitted, the lender will verify the information provided by the applicant.

- Verification may involve checking credit scores, employment status, income verification, and other relevant details.

Approval Process

- If the information provided meets the lender’s criteria, the application is approved.

- Approval for instant loans is usually quick, with funds disbursed within a short period after approval.

Interest Rates and Fees

When considering instant loans, it is crucial to understand the interest rates and fees associated with them. These factors can significantly impact the overall cost of borrowing money.

Comparing Interest Rates

Interest rates for instant loans can vary widely depending on the lender and the type of loan. It is essential to compare rates from different lenders to ensure you are getting the best deal. Some lenders may offer lower interest rates for borrowers with a good credit score, while others may have fixed rates for all customers.

Common Fees

There are several common fees associated with instant loans, including origination fees, late payment fees, and prepayment penalties. These fees can add to the overall cost of the loan and should be considered when comparing loan options. Origination fees are typically charged upfront and are a percentage of the total loan amount. Late payment fees are incurred if you miss a payment, and prepayment penalties are charged if you pay off the loan early.

Tips for Finding the Best Rates and Fees

- Shop around and compare rates from multiple lenders to find the most competitive offer.

- Check your credit score and work on improving it to qualify for lower interest rates.

- Read the fine print and understand all the fees associated with the loan before signing any agreements.

- Avoid loans with high origination fees or prepayment penalties to save on costs.

- Consider using a loan comparison website to easily compare rates and fees from different lenders.

Repayment Options

When it comes to repaying instant loans, borrowers have several options to choose from based on their financial situation and preferences. It’s essential to understand these repayment terms and options to ensure timely payments and avoid any negative consequences.

Flexible Repayment Plans

- Many instant loan providers offer flexible repayment plans, allowing borrowers to customize their repayment schedule based on their income and budget.

- Borrowers can choose to repay the loan in equal installments over a specific period or opt for a balloon payment at the end of the loan term.

- Some lenders also offer the option to make early repayments without incurring any prepayment penalties, helping borrowers save on interest costs.

Automatic Payment Deductions

- Another popular repayment option is setting up automatic payment deductions from the borrower’s bank account.

- This ensures that payments are made on time each month, reducing the risk of missed or late payments.

- Automatic payments can help borrowers stay on track with their repayment schedule and avoid any negative repercussions.

Consequences of Missing Loan Repayments

- Missing loan repayments can have serious consequences, including late fees, increased interest rates, and damage to the borrower’s credit score.

- Defaulting on an instant loan can lead to legal action, such as wage garnishment or asset seizure, to recover the outstanding amount.

- It’s crucial for borrowers to communicate with their lender if they are facing difficulty making payments to explore alternative solutions and avoid defaulting on the loan.

Strategies for Managing Loan Repayments

- Creating a budget and prioritizing loan repayments can help borrowers manage their finances effectively and ensure timely payments.

- Setting up reminders or automatic alerts for upcoming payments can help borrowers stay organized and avoid missing deadlines.

- If facing financial difficulties, borrowers should reach out to their lender immediately to discuss possible options, such as restructuring the loan or adjusting the repayment schedule.

Final Conclusion

Exploring instant loans reveals a world of quick financial options with varying interest rates, fees, and repayment terms. Make informed decisions and manage your instant loans effectively with the insights provided in this guide.